Author: admin

MANDARIN – 2026 e-Invoice Update in Malaysia: When Does It Actually Start?

2026 年马来西亚 e-Invoice 最新更新:到底什么时候开始?

图画版

###(实行日期不变,只是宽限期延长)

近期 LHDN 发布了关于 电子发票(e-Invoice) 的最新公告。

不少企业一看到 “延期 / Relaxation” 的字眼,就误以为:

e-Invoice 不用做了。

👉 事实上,这是一个 常见但错误的理解。

我们先把重点说清楚:

✅ e-Invoice 仍然照常在 2026 年 1 月 1 日开始执行

✅ 只是 宽限期(无罚款期)延长至 2027 年 1 月 1 日

✅ 2026 年是「练习年」,不是「不用做的一年」

公司到底什么时候需要开始做 e-Invoice?

是否需要执行 e-Invoice,不能只看年份,而是要同时看以下两个关键因素:

1️⃣ 公司开始营业的年份(Operation Year)

2️⃣ 公司的年营业额(Annual Sales)

以下为目前适用的执行标准说明。

一、2022 年或之前已开始营业的公司

⚠️ 若公司在 2022 年曾更改会计年度,营业额需换算为 12 个月

情况一

2022 年营业额超过 RM1,000,000(RM100 万)

➡️ 必须在 2026 年 1 月 1 日起执行 e-Invoice

情况二

2022–2025 年期间,每一年营业额都未超过 RM1,000,000

➡️ 暂时豁免(Exempted)

二、2023–2025 年期间才开始营业的公司

情况一

在 2023–2025 期间,有任何一年营业额超过 RM1,000,000

➡️ 从 2026 年 7 月 1 日开始执行 e-Invoice

情况二

期间内每一年都未超过 RM1,000,000

➡️ 暂时豁免(Exempted)

2026 年官方 Relaxation Period(一定要知道的重点)

LHDN 针对 2026 年,正式给予企业更大的缓冲空间与操作弹性,重点包括:

1️⃣ e-Invoice Phase 4(年营业额 RM100 万 – RM500 万)

原本的宽限期:6 个月

✅ 延长至 12 个月(无罚款)

2️⃣ 2026 年内允许的简化做法

在 2026 年期间,企业可:

使用 合并电子发票(Consolidated e-Invoice)

Self-Billed e-Invoice 也可合并开立

发票说明(Description)可使用 “Monthly Sales”

👉 目的是让企业先把系统和流程跑顺,而不是一开始就被处罚。

3️⃣ 建材 / 五金行业特别说明

单笔交易超过 RM10,000

➝ 必须开立 独立 e-Invoice其他交易

➝ 可使用 合并电子发票(Consolidated e-Invoice)

这个Announcement真正想传达什么?

这次的 announcement 不是在说「不用做 e-Invoice」,

而是在告诉企业:

👉 你有时间,把流程、系统和内部操作准备好。

真正聪明的老板,

不是想办法拖延或逃避 e-Invoice,

而是 善用 2026 年的缓冲期,把账务流程整理好,

避免未来被追溯、被罚款、甚至被查账。

2026 e-Invoice Update in Malaysia: When Does It Actually Start?

2026 e-Invoice Update in Malaysia: When Does It Actually Start?

中文版

(Implementation Date Remains the Same — Only the Grace Period Is Extended)

Following the latest announcement by LHDN, many businesses mistakenly assume that the extension or “relaxation” means e-Invoice is no longer required.

👉 This is incorrect.

Let’s clarify the key points first:

✅ e-Invoice implementation still starts on 1 January 2026

✅ The penalty-free transition period has been extended until 1 January 2027

✅ 2026 is a “practice year”, not a year where e-Invoice can be ignored

When Is Your Company Required to Implement e-Invoice?

e-Invoice implementation is determined by two key factors:

Your company’s operation year, and

Your annual sales turnover

Below is the current applicable framework.

1. Companies That Started Operations in 2022 or Earlier

⚠️ If your company changed its financial year in 2022, annual sales must be adjusted to a 12-month basis.

Scenario A

Annual sales in 2022 exceeded RM1,000,000 (RM1 million)

➡️ Mandatory implementation from 1 January 2026

Scenario B

Annual sales did not exceed RM1,000,000 for every year from 2022 to 2025

➡️ Temporarily exempted

2. Companies That Started Operations Between 2023 and 2025

Scenario A

Annual sales exceeded RM1,000,000 in any year between 2023 and 2025

➡️ Implementation starts from 1 July 2026

Scenario B

Annual sales did not exceed RM1,000,000 in all those years

➡️ Temporarily exempted

Key Highlights of the 2026 Relaxation Period

LHDN has officially introduced several measures in 2026 to ease implementation and allow businesses sufficient time to adjust.

1️⃣ e-Invoice Phase 4 (RM1 million – RM5 million turnover)

Original penalty-free period: 6 months

✅ Extended to 12 months (no penalties)

2️⃣ Flexibilities Allowed During 2026

Throughout 2026, businesses are allowed to:

Issue Consolidated e-Invoices

Consolidate Self-Billed e-Invoices

Use simplified descriptions such as “Monthly Sales”

The objective is to allow businesses to stabilise their systems and workflows before full enforcement.

3️⃣ Special Industry Rule: Building Materials & Hardware Suppliers

Single invoice above RM10,000

➝ Must issue an individual e-InvoiceOther transactions

➝ Allowed to issue Consolidated e-Invoices

What Does This Announcement Really Mean?

This announcement does not mean e-Invoice is optional.

Instead, it means:

👉 Businesses are given additional time to prepare, refine processes, and ensure compliance.

Smart business owners are not looking for ways to avoid e-Invoice —

they use the 2026 transition period to organise systems, accounting processes, and internal controls properly, avoiding future penalties or audit risks.

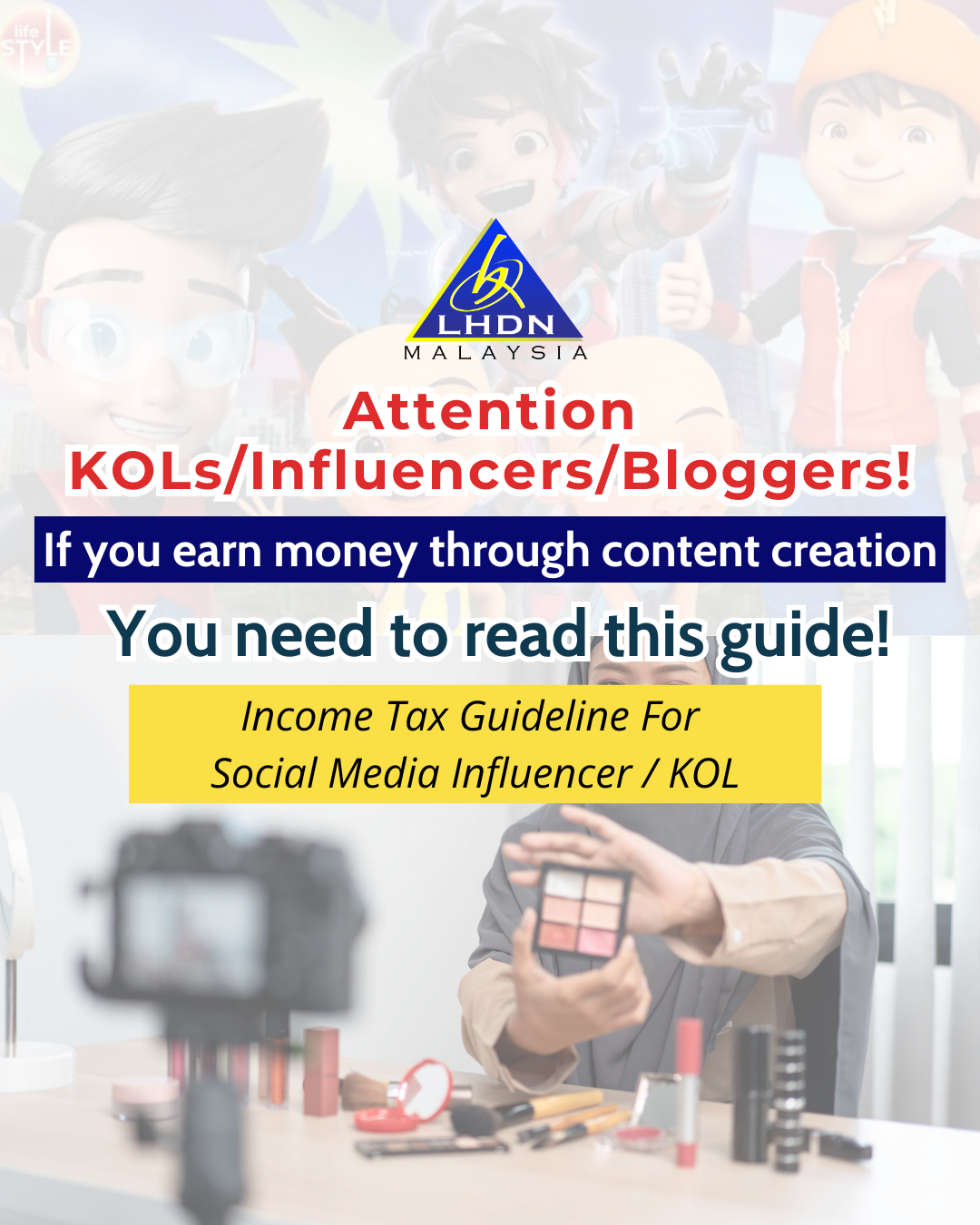

KOL & Influencer Tax in Malaysia Illustration

KOL & Influencer Tax in Malaysia: Explained LHDN Official Guideline (Illustration) - ENG

马来西亚 KOL / 网红税务指南 (图文版) - 中文

马来西亚 KOL / 网红税务指南

马来西亚 KOL / 网红税务指南:LHDN 官方文件一次讲清楚

近期「KOL / 网红要交税」在马来西亚引起热议,许多人误以为 从 YA2026 才开始需要报税。

事实上,LHDN 于 2026 年 1 月 14 日发布的《社交媒体影响者收入税务处理指南》并不是新法律,也不是 Gazetted Order。

这份指南的目的,是解释现有《1967 年所得税法》如何适用于 KOL / Influencer 收入。

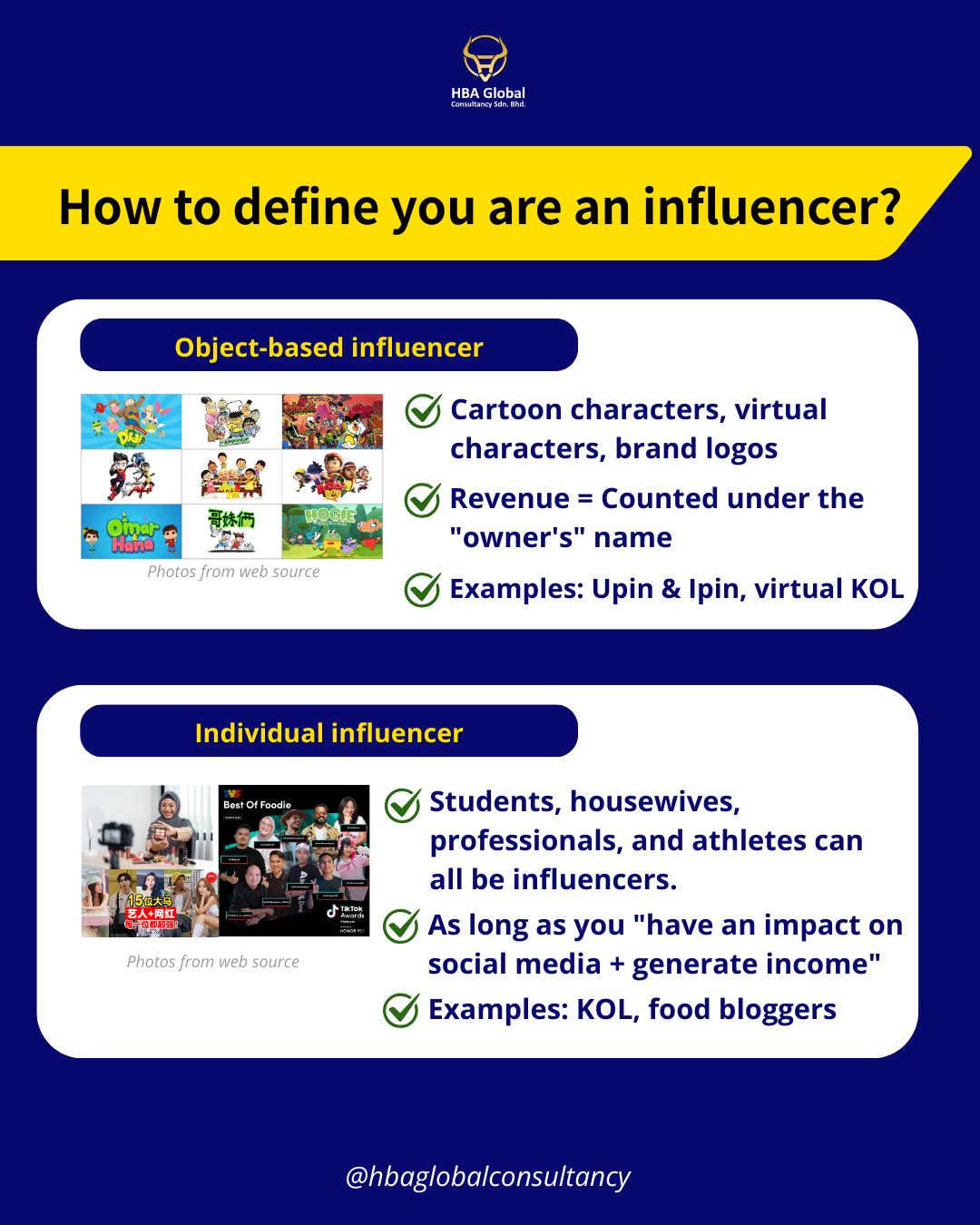

谁被视为社交媒体影响者?

根据 LHDN,凡是通过以下活动获取收入者,皆可能被视为 Influencer:

制作或发布内容(视频、音频、文字)

在社交媒体上推广产品或服务

参与线上或线下活动

因影响力而获得报酬、赠品或好处

粉丝数量并不是判断标准。

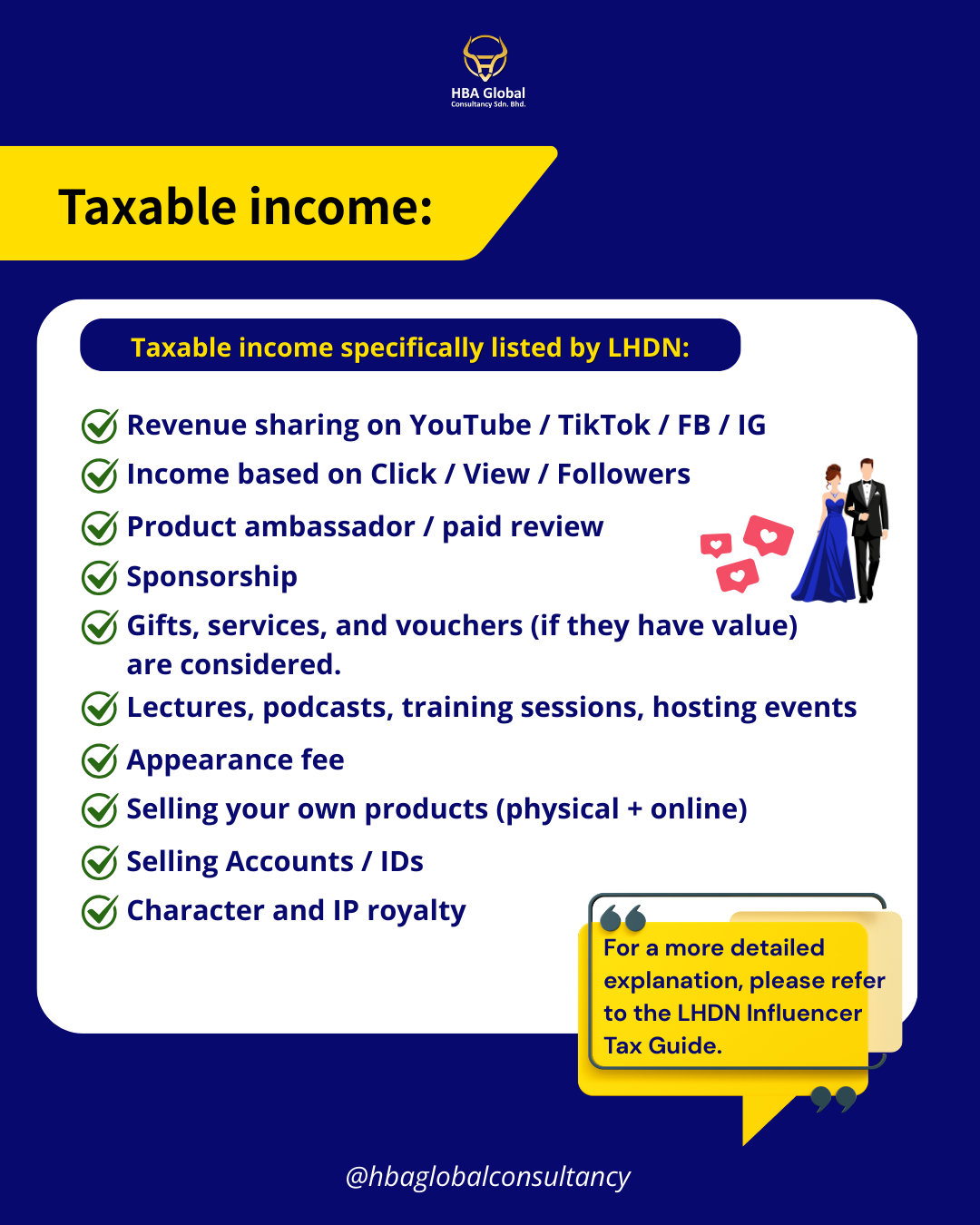

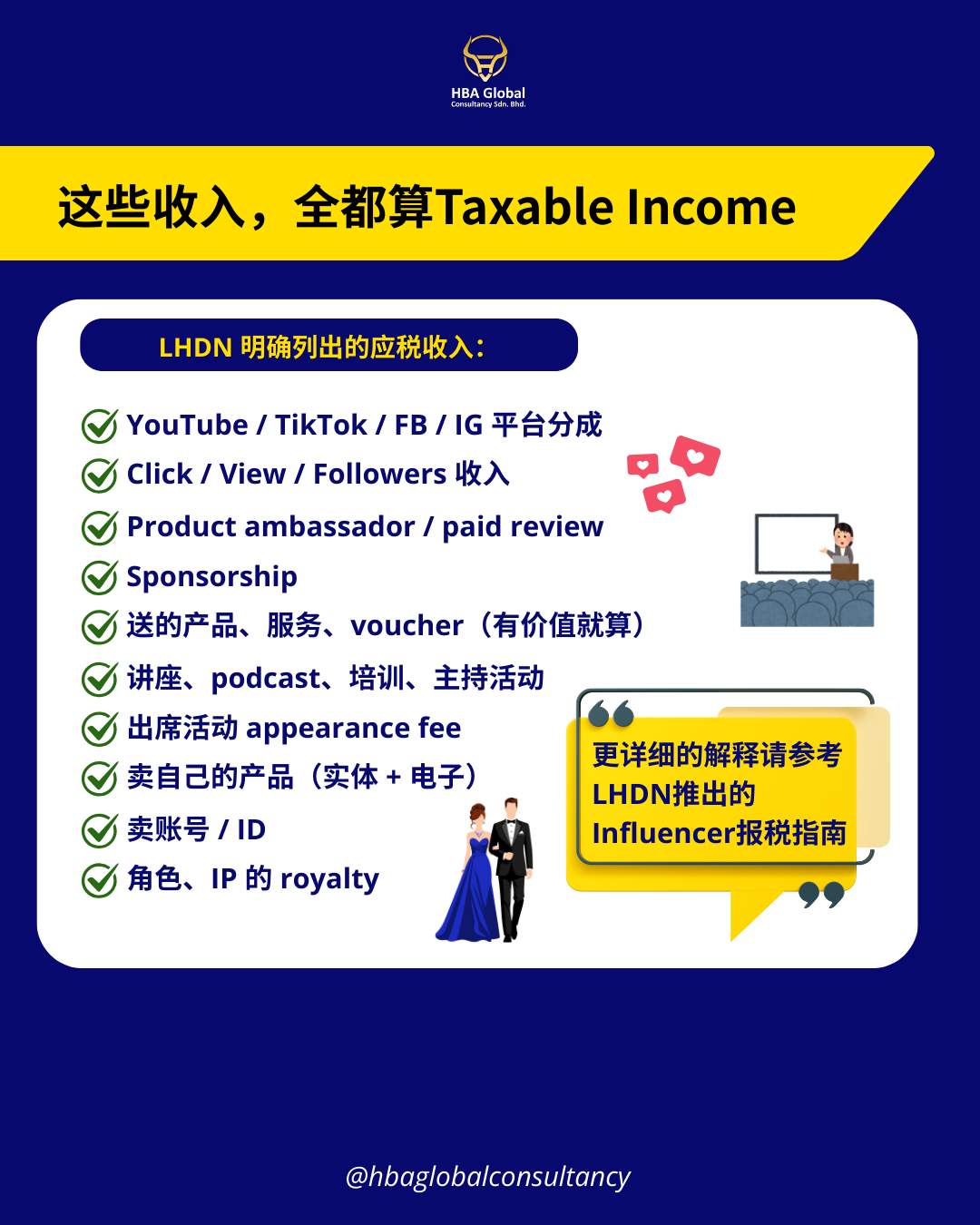

哪些收入需要报税?

KOL / 网红收入被视为 专业收入(Paragraph 4(a)),包括现金与非现金收入:

✔ 平台收入

YouTube / Facebook / Instagram / TikTok

广告费、点击费、观看次数分成

Affiliate 或订阅收入

✔ 品牌合作

合作费用

免费产品、服务、住宿、机票

折扣、代金券或其他有价值的好处

✔ 销售与专业活动

自有商品或线上课程

演讲、主持、活动出席费

⚠️ 即使没有正式合约,只要因推广而获得的收入,都必须申报。

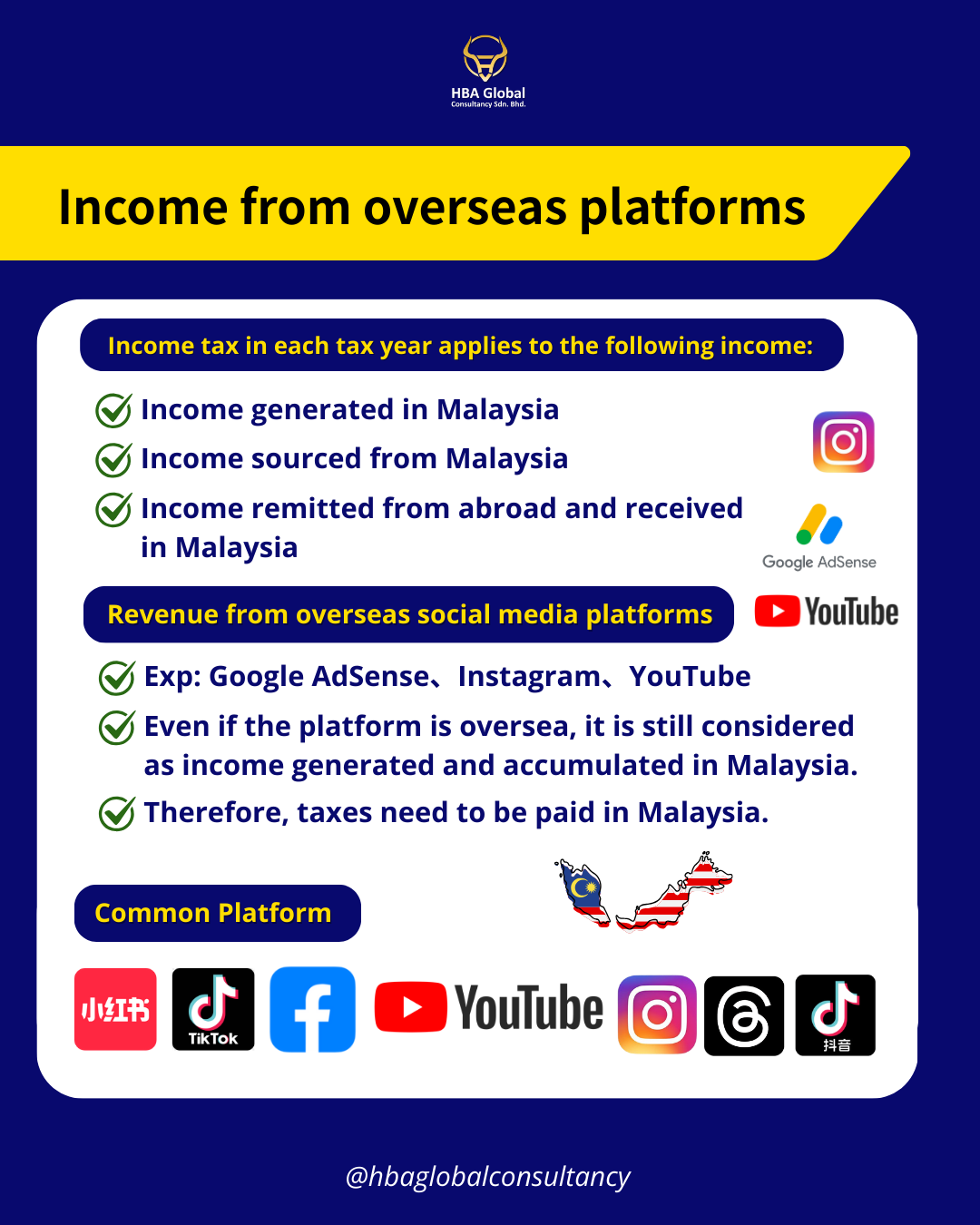

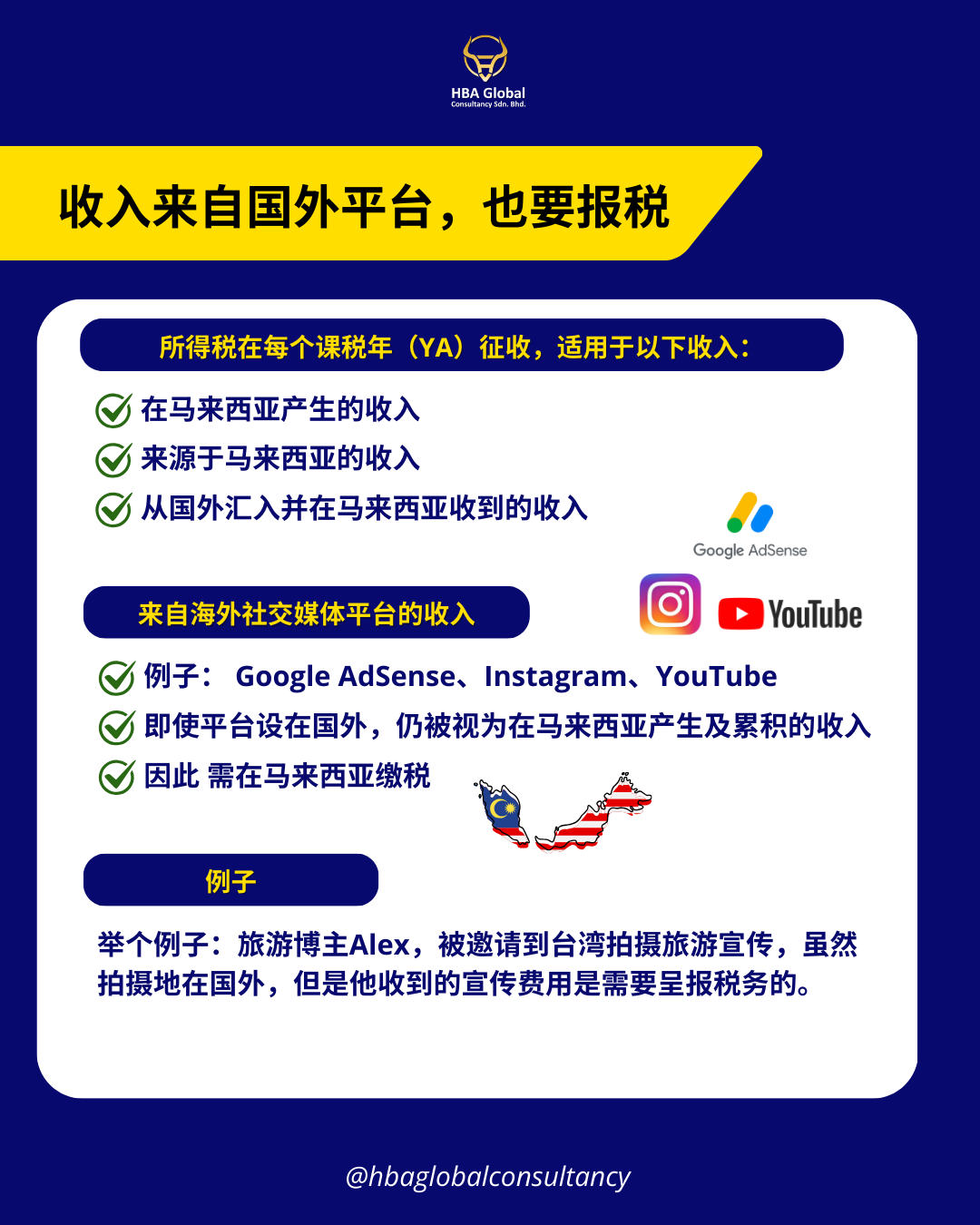

海外平台收入要报税吗?

要。

即使收入来自海外平台或外国公司,只要 Influencer 的活动是在马来西亚进行,该收入仍视为源自马来西亚,需在本地报税。

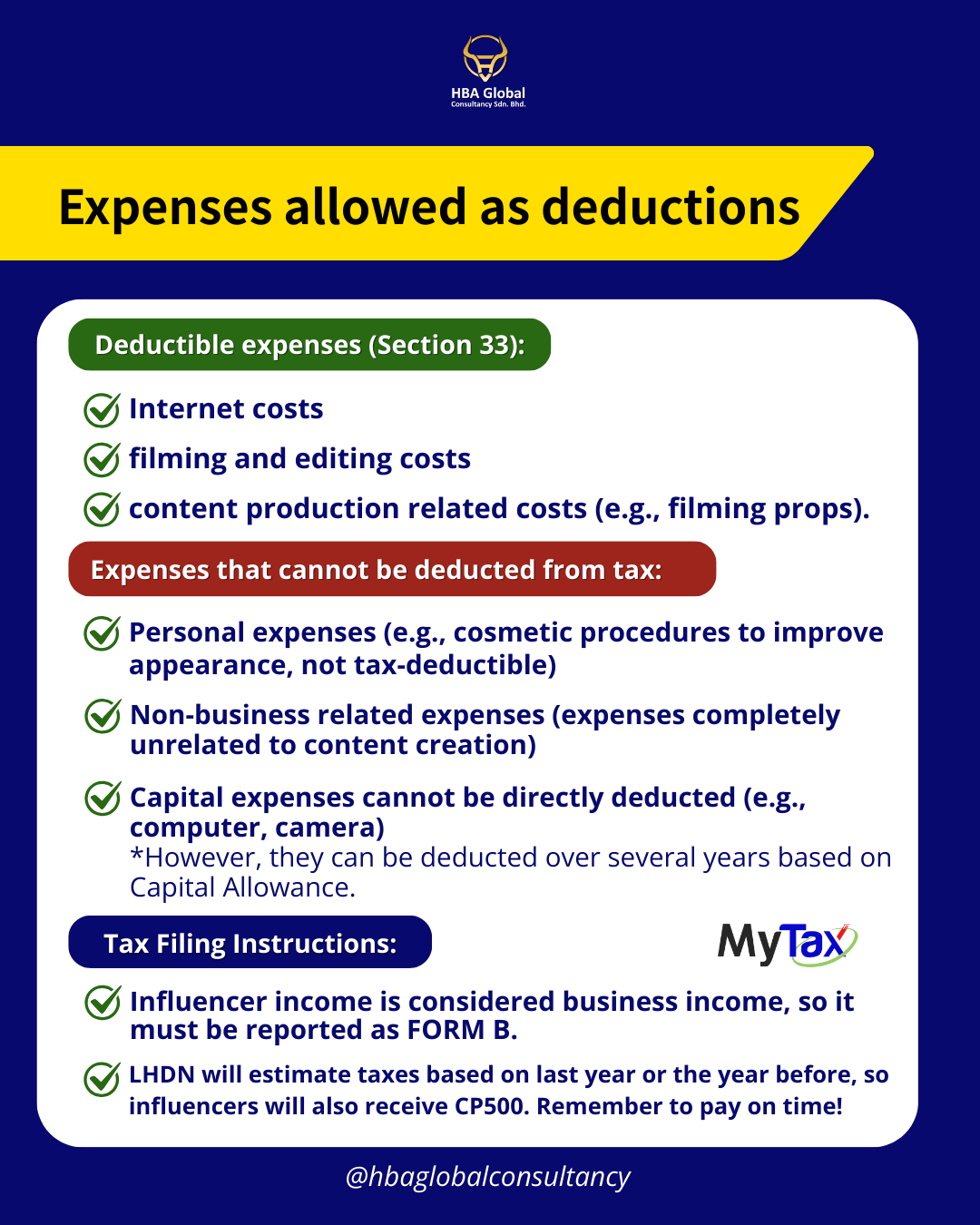

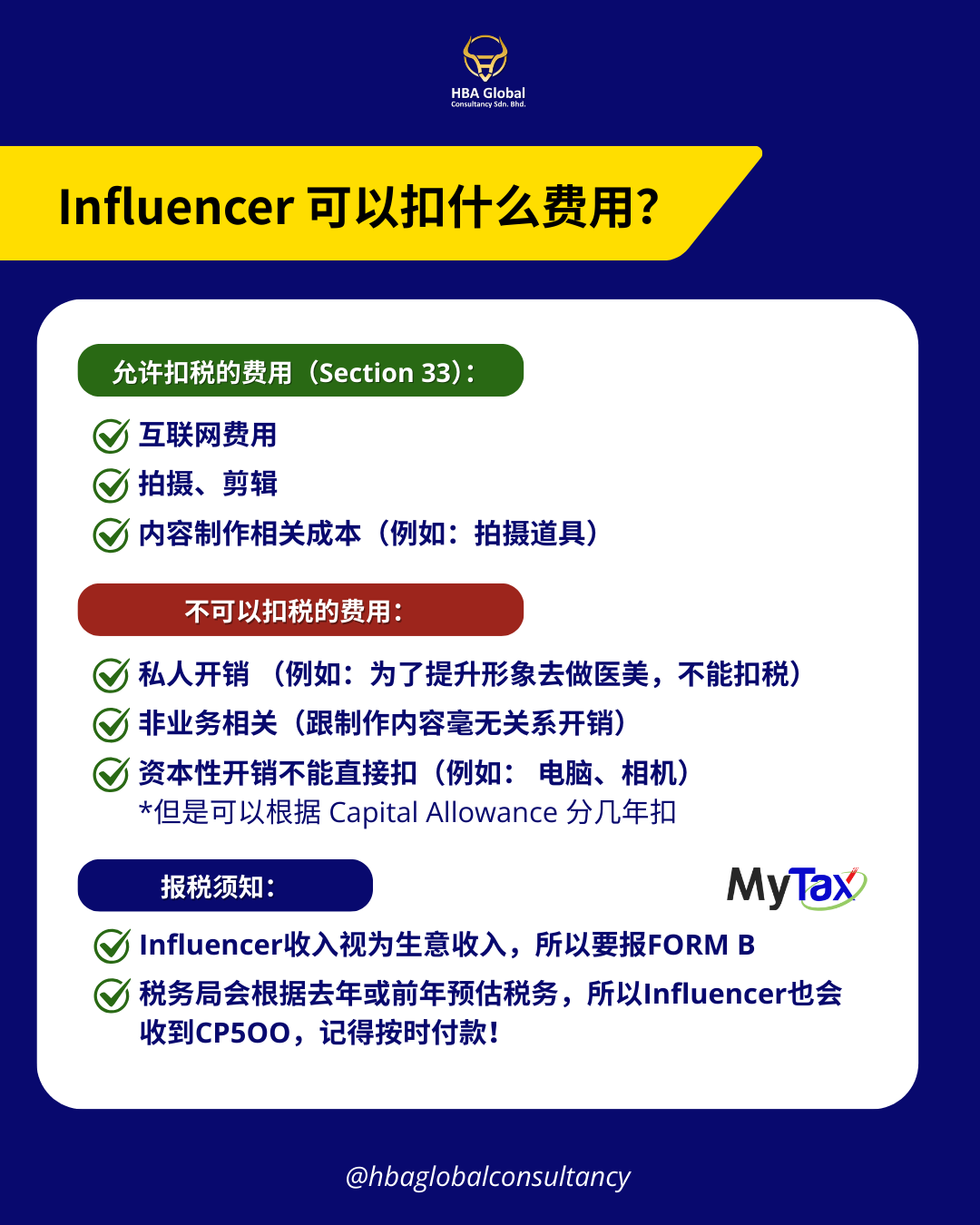

可扣税费用与资本津贴

只要是 完全与收入产生有关的费用,可作为扣税项目,例如:

网络费用

拍摄与剪辑成本

内容制作相关开销

相机、设备等资本性支出,若符合条件,可申请资本津贴。

报税责任与记录保存

Influencer 需注意:

CP500 分期缴税

正确估算税额

至少保存 7 年 的收入与费用记录

多数问题并非逃税,而是 没有记录、资料不完整。

总结

这份 LHDN 指南 不是新税制,

而是让 KOL / Influencer 更清楚如何合规申报。

重点不是「怕」,

而是 清楚、提早、正确。

KOL & Influencer Tax in Malaysia 2026

KOL & Influencer Tax in Malaysia: Explained LHDN Official Guideline (Complete Guide)

中文版

Introduction

In Malaysia, tax treatment for KOLs and social media influencers has recently become a trending topic. Many content creators believe that influencer tax only starts from YA 2026, but this understanding is not accurate.

On 14 January 2026, LHDN issued the Guidelines on Tax Treatment on Income of Social Media Influencer.

It is important to note that this document is a guideline, not a new law or gazette order.

The purpose of this guideline is to clarify how existing provisions of the Income Tax Act 1967 apply to influencer income, not to introduce new tax obligations.

Who Is Considered a Social Media Influencer?

According to LHDN, a social media influencer is any individual or entity that earns income by:

Producing or uploading content (video, audio, written content)

Appearing in events or programmes on social media

Promoting products, brands, or services

Receiving payments, gifts, or benefits due to their social media influence

This definition applies regardless of follower count and includes professionals, artists, athletes, students, and business owners.

Types of Influencer Income That Are Taxable

LHDN clearly states that influencer income is taxable under Paragraph 4(a) of the Income Tax Act 1967 as income from a profession.

Taxable income includes both cash and non-cash receipts, such as:

1. Direct payments from platforms

YouTube, Facebook, Instagram, TikTok monetisation

Payment per view, click, follower, or advertisement

Affiliate or subscription-based commissions

2. Brand collaborations & ambassadorships

Cash payments for promotion or reviews

Free products, vouchers, services, discounts, or facilities

Sponsored travel, accommodation, or experiences

3. Sale of goods or services

Physical products

Digital products (e-books, courses, online training)

4. Appearance & professional fees

Speaking engagements, seminars, podcasts

Event appearances, judging roles, hosting fees

Important:

Even if there is no written contract, income received in exchange for promotional activities must still be declared.

Income from Overseas Platforms: Is It Taxable?

Yes.

LHDN clarifies that income received from foreign platforms (e.g. Google AdSense, Meta, overseas brands) is still taxable in Malaysia if the influencer’s activities are carried out in Malaysia.

The location of payment or platform does not override where the influencer operates from.

Allowable Expenses & Capital Allowances

Influencers are allowed to deduct expenses that are wholly and exclusively incurred in producing income, such as:

Internet and data costs

Filming, editing, and production expenses

Platform-related operational costs

Capital allowances may also be claimed on qualifying assets (e.g. cameras, equipment) under Schedule 3 of the Income Tax Act, subject to conditions.

Personal or capital expenses that are not related to income production are not deductible.

Tax Responsibilities & Record Keeping

Influencers with non-employment income are subject to:

CP500 tax instalments under Section 107B

Proper estimation and timely payment

Record keeping for at least 7 years, including:

Income records

Collaboration proof

Supporting documents for expenses

Most tax issues arise not from tax evasion, but from poor documentation and inconsistent reporting.

Key Takeaway

The LHDN guideline does not create new tax rules.

It explains how existing tax laws already apply to social media influencer income.

If you earn income through social media, compliance is about:

✔ Understanding what counts as income

✔ Declaring correctly

✔ Keeping proper records

Early clarity helps avoid penalties and unnecessary audit risks.

Disclaimer:

The information shared in this post is for general educational and reference purposes only. It does not constitute professional advice. Regulations and requirements may change from time to time. For guidance specific to your situation, please consult with our firm or a qualified professional.

Understanding Form EA: Your Annual Tax Guide

Understanding Form EA: Your Annual Tax Guide

Every year, as the calendar turns to January, the Malaysian tax season begins. For both employers and employees, the most significant document during this period is the Form EA.

At HBA Accounting House, we receive many questions about this form. Here is everything you need to know about what it is and the critical timeline you must follow every year.

What is Form EA?

Form EA (also known as the Annual Remuneration Statement) is a document that private-sector employers must prepare for their employees.

It acts as a comprehensive summary of all earnings and deductions for the preceding calendar year (January 1st to December 31st). It includes:

Gross Salary & Wages: Your basic pay and overtime.

Bonuses & Commissions: Any additional incentives earned.

Allowances: Transport, parking, or meal allowances.

Statutory Contributions: The total amount of EPF, SOCSO, and EIS deducted.

Monthly Tax Deductions (PCB): The total tax already remitted to LHDN on your behalf.

Why is it used every year? > Employees cannot file their personal income tax (Form BE/B) without the figures from Form EA. It is the "source of truth" used to fill out the LHDN e-Filing system accurately.

The Annual Timeline: Key Dates to Remember

The Form EA cycle follows a strict schedule set by the Inland Revenue Board of Malaysia (LHDN). Mark these recurring dates in your calendar:

Why the February 28th Deadline Matters

By law (Section 83(1A) of the Income Tax Act 1967), employers must provide the Form EA to their employees on or before the last day of February every year.

Failing to meet this deadline is a serious offense. Employers can face fines ranging from RM200 to RM20,000, or even imprisonment, for failing to provide this form to their staff on time.

Summary for Employees

Even if you resigned midway through the year, your former employer is still legally required to issue you a Form EA for the period you were with them. Ensure you gather all your Form EAs if you changed jobs during the year!

Need Professional Tax Assistance?

Staying compliant with LHDN requirements doesn't have to be stressful. At HBA Accounting House, we specialize in payroll management and tax compliance to ensure your business never misses a deadline.

Disclaimer:

The information shared in this post is for general educational and reference purposes only. It does not constitute professional advice. Regulations and requirements may change from time to time. For guidance specific to your situation, please consult with our firm or a qualified professional.

Form E: The Essential Annual Return for Employers

Form E: The Essential Annual Return for Employers

If you own a business in Malaysia, Form E is a mandatory reporting requirement that cannot be ignored. Even if your company is dormant or has no employees, you likely still have a responsibility to file.

What is Form E?

Form E (the Return Form of Employer) is a declaration submitted by an employer to the Inland Revenue Board of Malaysia (LHDN).

Unlike the Form EA, which is handed to your staff, the Form E is submitted directly to LHDN. It serves as a summary of:

The total number of employees you had during the year.

The total amount of remuneration (salaries, bonuses, etc.) paid.

The total amount of Monthly Tax Deductions (PCB/MTD) remitted to LHDN.

Confirmation that you have issued Form EA to all your employees.

The "Silent Partner": What is C.P. 8D?

You cannot mention Form E without mentioning C.P. 8D. This is the detailed list of every single employee’s salary and deduction info. For the Form E submission to be considered "complete," you must also submit the C.P. 8D data (usually via the e-Data Praisi system or by uploading a file in the e-Filing portal).

The Annual Timeline: Don't Miss the Grace Period

The timeline for Form E is slightly different from Form EA, providing employers a bit more time to consolidate their data.

Important for 2026:

As we look toward the 2026 tax season (reporting for the 2025 calendar year), your digital submission via the MyTax portal must be completed by 30 April 2026.

Who Must File?

A common mistake is thinking you only file if you have taxable employees.

Sdn Bhd / Berhad / LLP: Must file every year, even if there are zero employees (a "NIL" return).

Sole Proprietors / Partnerships: Must file if they have at least one employee.

The Risk of Non-Compliance

Missing the Form E deadline is a serious offense under the Income Tax Act 1967. Penalties for failing to submit or late submission can range from RM200 to RM20,000, and LHDN can also take legal action against company directors.

Disclaimer:

The information shared in this post is for general educational and reference purposes only. It does not constitute professional advice. Regulations and requirements may change from time to time. For guidance specific to your situation, please consult with our firm or a qualified professional.

4 things you need to know about Self-billed e-Invoice in Malaysia

4 things you need to know about Self-billed e-Invoice in Malaysia

In Malaysia’s e-invoice framework, a Self-billed e-Invoice is a document issued by the Buyer (the person making the payment) rather than the Supplier. This is mandatory for specific transactions where the supplier is unable or not required to issue a validated e-invoice.

As of January 2026, here is the guide for handling Self-billed e-invoices.

1. When to Issue a Self-Billed e-Invoice

You must issue a self-billed e-invoice in the following scenarios:

2. Key Data Requirements

Unlike a standard invoice, the Buyer is the Issuer. You will need:

Supplier Information: Full legal name, address, and TIN (Tax Identification Number).

Note: For foreign suppliers, use the placeholder TIN: EI00000000030.

Buyer Information: Your own company details (automatically populated in the portal).

Transaction Details: Classification code, product description, quantity, unit price, and tax rate.

Customs Reference: For imports, include the Customs Form No. 1 or 9 (if applicable).

3. The Issuance Process (Step-by-Step)

You can issue these through the MyInvois Portal or an integrated API/Accounting Software.

Select Document Type: Choose Self-Billed Invoice (Document Type Code: 02).

Input Details: Enter the supplier's details. If they are a non-business individual, use their IC/Passport number.

Submission: Submit the document to IRBM (LHDN) for real-time validation.

Validation: LHDN issues a Unique Identifier Number (UIN) and a QR code.

Sharing: Once validated, you should share the human-readable version (PDF) with the supplier for their records.

4. Important Rules for 2026

Exemption Threshold: If your annual revenue is below RM1 million, you are generally exempt from issuing e-invoices until Phase 5 (July 2026).

Consolidation Limit: Effective 1 January 2026, any transaction exceeding RM10,000 cannot be consolidated; it must have an individual self-billed e-invoice.

Comparison: Standard vs. Self-Billed

Disclaimer:

The information shared in this post is for general educational and reference purposes only. It does not constitute professional advice. Regulations and requirements may change from time to time. For guidance specific to your situation, please consult with our firm or a qualified professional.

Supplier Information: Full legal name, address, and TIN (Tax Identification Number).

Note: For foreign suppliers, use the placeholder TIN: EI00000000030.

Buyer Information: Your own company details (automatically populated in the portal).

Transaction Details: Classification code, product description, quantity, unit price, and tax rate.

Customs Reference: For imports, include the Customs Form No. 1 or 9 (if applicable).

Select Document Type: Choose Self-Billed Invoice (Document Type Code: 02).

Input Details: Enter the supplier's details. If they are a non-business individual, use their IC/Passport number.

Submission: Submit the document to IRBM (LHDN) for real-time validation.

Validation: LHDN issues a Unique Identifier Number (UIN) and a QR code.

Sharing: Once validated, you should share the human-readable version (PDF) with the supplier for their records.

Exemption Threshold: If your annual revenue is below RM1 million, you are generally exempt from issuing e-invoices until Phase 5 (July 2026).

Consolidation Limit: Effective 1 January 2026, any transaction exceeding RM10,000 cannot be consolidated; it must have an individual self-billed e-invoice.

How to Check CP500 and Pay?

")

After receiving the CP500 installment notice, not sure how to pay? 😟 Don’t worry! We have compiled detailed steps for your reference! ✅

老板们收到CP500分期通知后不清楚要怎么支付?😟 别担心!我们整理了详细步骤让你们参考!✅

Step 1 第一步

After logging into MyTax, click CP500

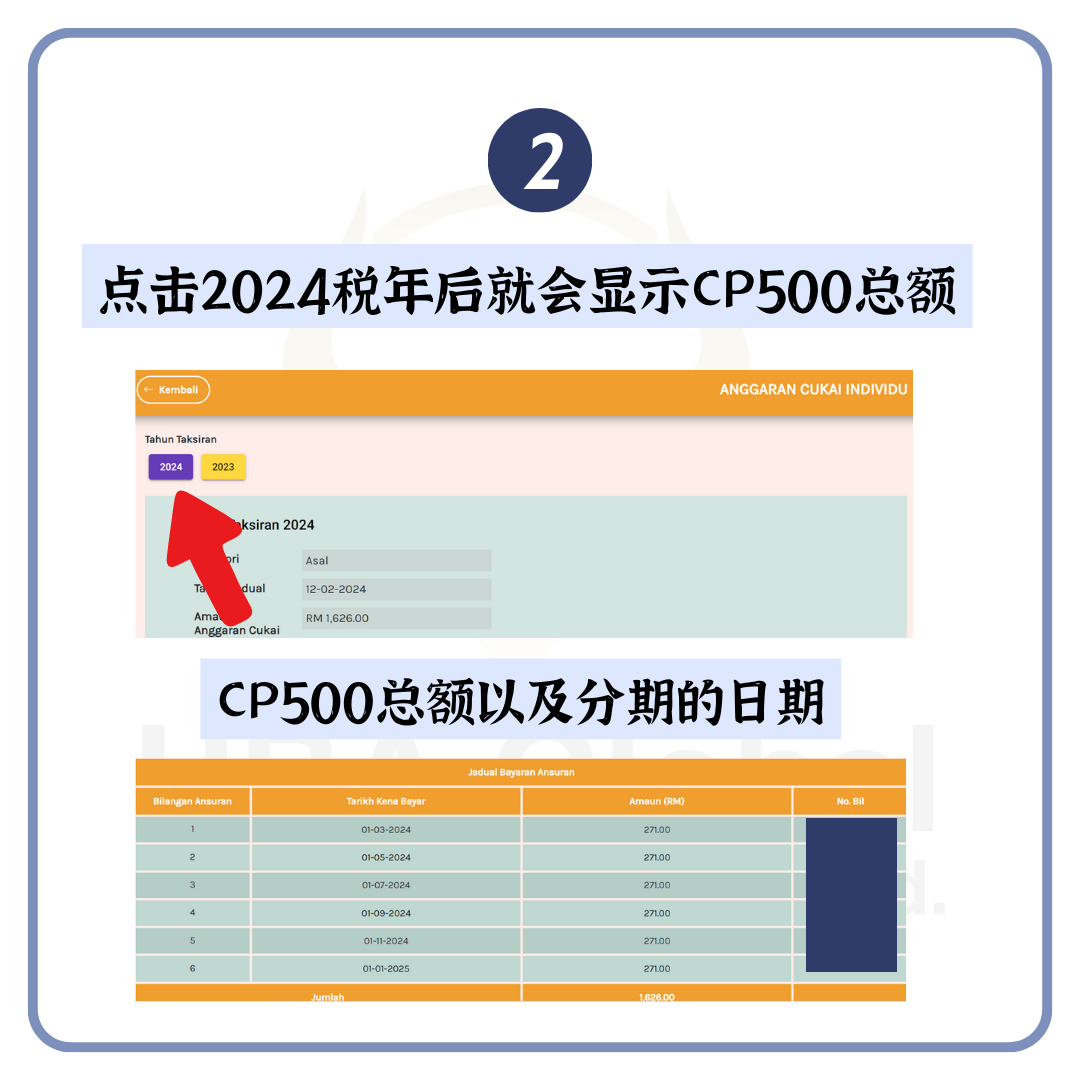

Step 2 第一步

Click on the 2024 tax year and the total CP500 installment date will be displayed.

Step 3 第三步

Click "Paparan Bill" to pay

Step 4 第四步

Click on the bill you want to pay. After confirmed the amount, click "Teruskan".

Step 5 第五步

After checking that the information and amounts are correct, click "Teruskan"

Step 6 第六步

After selecting the payment method, click "Teruskan"

Step 7 第六步

After confirming the payment information, click "Teruskan"

Step 8 第八步

The payment is successful if you come to this page!