As we move through 2026, many taxpayers may already be spending on items that qualify for tax relief without realizing it.

Every year, Malaysia's Budget introduces changes to personal income tax reliefs. Some updates receive significant attention, while others go unnoticed until tax filing season arrives.

By then, many taxpayers discover that receipts have been misplaced, e-Invoices cannot be found, or supporting documents are incomplete.

To help you prepare early, here are six notable tax relief updates introduced under Budget 2026.

1. Expanded Tax Relief for Vaccination Expenses

Previously, only selected vaccines qualified for tax relief.

For YA 2026, the scope has been expanded to include vaccines approved by the National Pharmaceutical Regulatory Agency (NPRA).

Examples include:

Influenza Vaccine

Dengue Vaccine

HPV Vaccine

Pneumococcal Vaccine

Other approved vaccines

This relief falls under the medical expenses category and may help reduce your taxable income when supported by proper documentation.

2. Day Care and Transit Centres Are Now Eligible

Working parents may benefit from this update.

Previously, tax relief was generally available for fees paid to registered childcare centres (TASKA) and kindergartens (TADIKA).

The relief now includes:

Day Care Centres

Transit Centres

This expansion provides additional support for parents who rely on after-school care services for their children.

Be sure to keep payment records and receipts issued by the childcare provider.

3. Children's Life Insurance and Takaful Now Qualify

One of the lesser-known updates involves life insurance tax relief.

Previously, the relief mainly covered insurance premiums relating to the taxpayer and spouse.

Under the updated rules, eligible premiums paid for children's life insurance and children's takaful plans may also qualify under the existing relief framework.

It is important to understand that this is not a new relief category. Instead, the scope of the existing relief has been expanded.

Parents are encouraged to retain policy documents and premium payment records for future tax filing purposes.

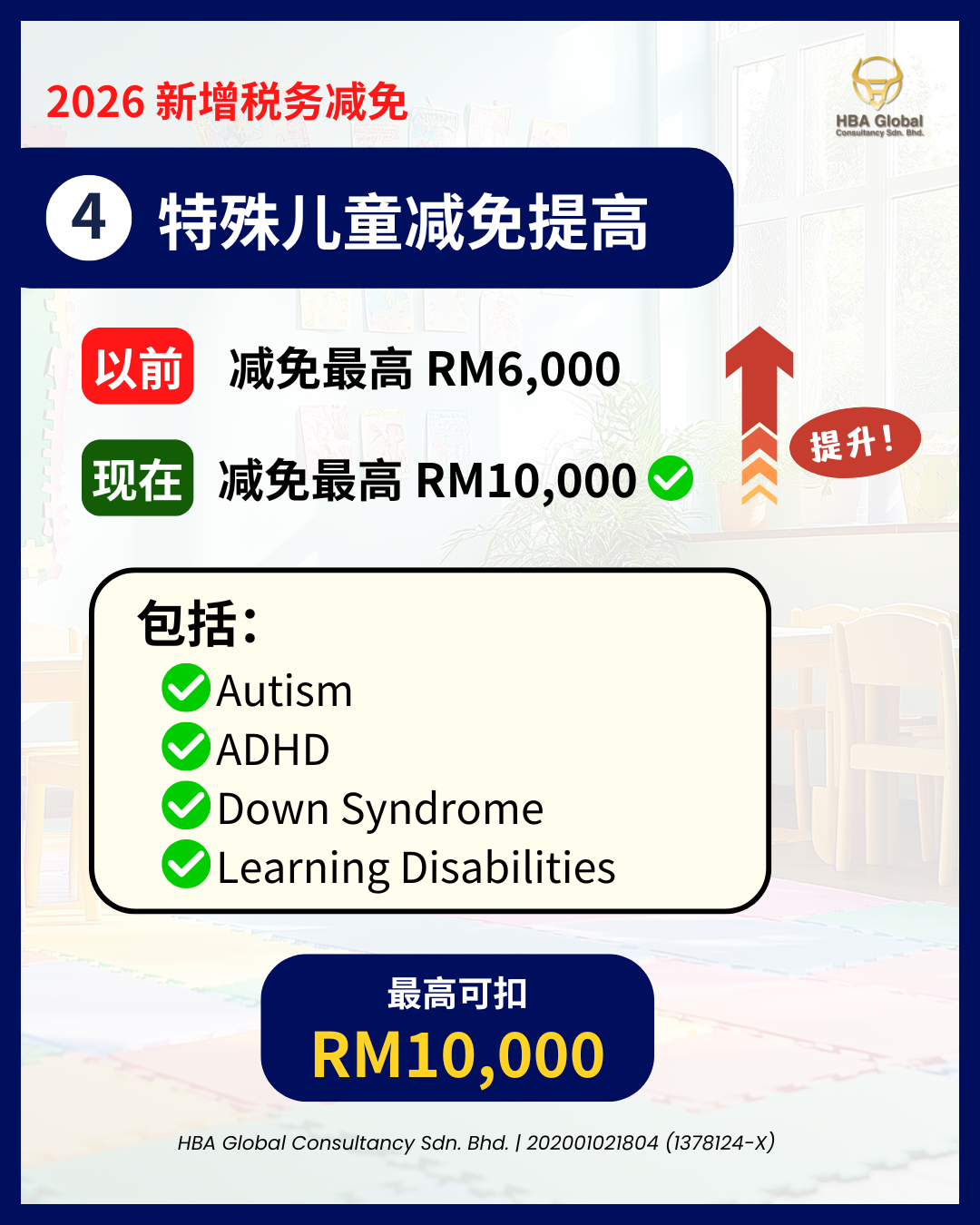

4. Higher Relief for Special Needs Children

Families caring for children with special needs will benefit from an increased relief amount.

The allowable relief has been increased from RM6,000 to RM10,000.

This applies to qualifying conditions such as:

Autism Spectrum Disorder (ASD)

Attention Deficit Hyperactivity Disorder (ADHD)

Down Syndrome

Global Developmental Delay (GDD)

Learning Disabilities

Other recognised developmental conditions

This enhancement reflects the government's continued effort to support families facing higher medical and educational expenses.

5. Home CCTV and Food Waste Grinders Added

Budget 2026 also introduces a practical update for homeowners.

The following items may now qualify under the relevant tax relief category:

Home CCTV Systems

Food Waste Grinders

These are in addition to previously eligible items such as electric vehicle chargers and food waste composting machines.

If you are planning home security or sustainability improvements, remember to retain the purchase invoice and installation records.

6. Selected Domestic Tourism Attractions May Qualify

In conjunction with Visit Malaysia Year 2026, selected tourism-related expenses may qualify for tax relief.

Examples include:

Theme Parks

Zoos

Museums

National Parks

Marine Parks

Cultural Programmes

Certain leisure activities may therefore contribute towards tax savings while supporting Malaysia's tourism industry.

Taxpayers should retain tickets, receipts, and payment records as supporting documents.

Why You Should Start Organising Your Receipts Now

One of the most common mistakes taxpayers make is waiting until tax filing season before reviewing their expenses.

By that time:

Receipts may have been misplaced

e-Invoices may have been deleted

Payment records may be difficult to retrieve

The best approach is to create a dedicated folder, either physical or digital, and store all relevant tax documents throughout the year.

Documents You Should Keep

For YA 2026, consider keeping records for:

Vaccination Expenses

Childcare and Transit Centre Fees

Children's Insurance Premiums

Special Needs Child Treatment Expenses

Home CCTV Purchases

Domestic Tourism Attraction Tickets

e-Invoices

Payment Receipts

Under Malaysian tax regulations, supporting documents should generally be retained for at least seven years.

Final Thoughts

Tax reliefs may seem like a small part of financial planning, but they can significantly reduce your taxable income when utilised correctly.

The key is preparation.

Understanding the available tax reliefs now allows you to make informed spending decisions and avoid missing out on legitimate tax savings later.

If you are unsure whether a particular expense qualifies for tax relief, it is always advisable to seek professional tax advice before filing your tax return.

Need Help With Personal Tax Planning?

At HBA Global Consultancy, we assist individuals and businesses in understanding their tax obligations while maximising available tax reliefs in compliance with LHDN requirements.

With more than 12 years of experience and nearly 800 businesses served, our team is ready to help.

✔ Accounting

✔ Tax

✔ Company Secretary

✔ Audit

Contact us today to learn more.

Disclaimer

The information provided in this article is intended for general educational and informational purposes only. While every effort has been made to ensure the accuracy of the information at the time of publication, tax laws, reliefs, eligibility criteria, administrative practices, and implementation guidelines may be revised, updated, or clarified by the Inland Revenue Board of Malaysia (LHDN) from time to time.

The tax reliefs, limits, examples, and explanations discussed in this article are based on publicly available information relating to Budget 2026 proposals and announcements. The actual eligibility, qualifying conditions, supporting documentation requirements, and claim procedures may vary depending on an individual's circumstances and the latest guidance issued by LHDN.

Readers are strongly advised to refer to the latest official publications, guidelines, FAQs, Public Rulings, and announcements issued by LHDN before making any tax-related decisions or submitting their income tax returns.

This article should not be construed as tax, legal, financial, or professional advice. HBA Global Consultancy Sdn. Bhd. shall not be held responsible for any loss, liability, or consequences arising from reliance on the information contained in this article without obtaining professional advice tailored to specific circumstances.

For the most up-to-date information, please refer directly to LHDN's official website and published guidance.

")

")

")