更新日期:2026 年 7 月 13 日

马来西亚人力资源部与 PERKESO 最近宣布调整 LINDUNG 24 JAM/Skim Kemalangan Bukan Bencana Kerja(SKBBK) 的实施方式。

从即日起:

✅ 本地员工:自愿参与

✅ 外籍员工:维持强制参与

同时,PERKESO 已开放线上系统,让本地员工选择是否继续参与这项计划,并完成相关声明。

LINDUNG 24 JAM 是 PERKESO 推出的非工作相关意外保障计划,主要为符合资格的受雇员工提供工作时间以外的意外保障。

保障范围可能包括:

在家中发生的意外

非上下班途中发生的交通事故

周末或私人活动期间发生的意外

运动、休闲或日常生活中发生的意外

需要注意的是,这项计划主要保障 非工作相关意外。

如果意外是在工作期间发生,或与工作及上下班通勤有关,则一般属于原有的 Skim Bencana Pekerjaan(工伤保障计划) 范围。

LINDUNG 24 JAM 于 2026 年 6 月 1 日实施时,原本适用于符合条件的本地及外籍员工。

不过,人力资源部于 2026 年 7 月 9 日宣布:

本地员工不再被强制要求参与,可根据自己的保障需求和财务状况,自愿选择继续参与或退出。

外籍员工仍须继续参与,相关缴纳要求维持不变。

换句话说,本地员工现在拥有选择权,但外籍员工并不适用这项退出安排。

PERKESO 已开放线上系统,让员工选择:

选择:

“SAYA MEMILIH UNTUK MENYERTAI”

如果员工同时受雇于多名雇主,还需要选择由哪一名雇主负责处理该计划的缴纳。

选择:

“SAYA MEMILIH UNTUK TIDAK MENYERTAI”

选择退出的员工需要完成 Borang Perakuan Pelepasan Liabiliti(责任豁免声明)。

这份声明用于确认员工了解退出后的影响,包括一旦在非工作时间发生意外,将无法依据 LINDUNG 24 JAM 申请相关保障。

登入 PERKESO LINDUNG Faedah Portal:

https://lindungfaedah.perkeso.gov.my/auth/

首次使用者点击:

Daftar Akaun

然后填写:

姓名

身份证号码

电邮地址

密码

完成账号注册后,使用已登记的资料登入系统,并进入 LINDUNG 24 JAM 参与选择页面。

员工可选择:

✅ SAYA MEMILIH UNTUK MENYERTAI

表示继续参与计划

或

❌ SAYA MEMILIH UNTUK TIDAK MENYERTAI

表示不参与或选择退出计划

提交前,请仔细核对:

个人资料

身份证号码

雇主资料

所选择的参与状态

负责缴纳的雇主

确认所有资料正确后,完成线上声明并提交申请。

系统显示申请成功后,请下载并保存 Declaration Form/声明书。

建议再次检查声明书中的:

员工资料

雇主资料

参与或退出状态

提交日期

根据目前的线上指引,员工提交选择后,应将其视为正式声明。

因此,在按下确认前,请务必仔细检查所有资料及参与意愿,避免选错雇主或提交错误的参与状态。

员工也应了解:

继续参与,才可在符合条件的非工作相关意外发生时申请相关保障

选择退出后,将不再享有这项非工作意外保障

退出者需完成责任豁免声明

外籍员工不可选择退出

虽然参与决定由本地员工自行作出,但雇主和 HR 仍需要关注后续处理,包括:

提醒员工完成线上选择

保存员工提交的声明记录

确认 Payroll 系统中的参与状态

避免继续错误扣款或漏扣

妥善处理同时拥有多名雇主的员工

向员工说明参与与退出的实际影响

企业不应在没有员工正式声明的情况下,自行替员工决定参与状态。

LINDUNG 24 JAM 最初于 2026 年 6 月实施,因此部分雇主可能已经根据原有规定进行工资扣款。

对于后续 Payroll 调整、已扣除款项的处理方式,以及员工退出后的生效月份,企业应参考 PERKESO 最新系统指示和进一步公告。

建议 HR 与 Payroll 团队不要自行假设处理方式,以免出现少扣、重复扣款或错误退款的问题。

虽然本地员工现在可自愿选择,但这项计划仍提供工作时间以外的额外社会保障。

其主要作用包括:

扩大非工作相关意外的保障范围

在符合条件时提供医疗及相关福利

降低员工因私人意外而面对的财务压力

为没有私人意外保险的员工提供额外保障选择

员工在决定是否退出前,应先考虑自己现有的 Medical Card、Personal Accident Insurance、收入保障及家庭财务状况。

这次政策改变并不代表公司可以完全不处理。

企业仍应做到:

✅ 及时通知员工最新安排

✅ 指引员工使用官方系统

✅ 保存相关声明和记录

✅ 更新 Payroll 与 PERKESO 处理流程

✅ 区分本地员工与外籍员工

✅ 持续关注 PERKESO 后续公告

错误扣款、遗漏处理或没有保留员工声明,都可能为公司带来 Payroll 与合规风险。

LINDUNG 24 JAM 的最新安排可以简单理解为:

本地员工可从 2026 年 7 月 13 日起,通过 PERKESO 官方线上系统完成选择。

在提交前,员工应充分了解参与和退出的影响;雇主则应及时更新 Payroll 流程,并保存相关文件作为记录。

需要协助处理 Payroll、PERKESO、员工法定缴纳或 HR 合规事项?欢迎联系 HBA Global Consultancy 获取专业协助。

本文仅供一般资讯参考,不构成法律、人力资源、保险或专业合规意见。政策、系统流程及处理机制可能根据人力资源部或 PERKESO 的后续公告而调整。员工与雇主采取行动前,应以 PERKESO 最新官方资料为准。

图文版

Last Updated: 13 July 2026

Malaysia's Ministry of Human Resources (KESUMA) and the Social Security Organisation (PERKESO) have announced an important update to the implementation of the LINDUNG 24 JAM, also known as the Skim Kemalangan Bukan Bencana Kerja (SKBBK).

Effective immediately:

✅ Local employees – Participation is voluntary

✅ Foreign employees – Participation remains mandatory

At the same time, PERKESO has launched an online portal that allows eligible local employees to decide whether they wish to participate in the scheme and submit their declaration electronically.

LINDUNG 24 JAM (SKBBK) is a PERKESO social protection scheme that provides coverage for non-work-related accidents experienced by eligible employees outside of working hours.

Examples of situations that may fall under the scheme include:

Accidents at home

Road accidents unrelated to commuting to or from work

Weekend or personal activity accidents

Sports and recreational accidents

Other daily-life accidents outside the workplace

It is important to note that this scheme only covers non-work-related accidents.

Accidents arising out of employment or during commuting to and from work continue to be covered under PERKESO's Employment Injury Scheme (Skim Bencana Pekerjaan).

When LINDUNG 24 JAM was first introduced on 1 June 2026, participation was intended to apply to both local and foreign employees.

However, on 9 July 2026, the Ministry of Human Resources announced a policy revision.

Participation is no longer compulsory.

Eligible local employees may now decide whether they wish to:

Continue participating in the scheme; or

Opt out of the scheme.

The decision is entirely voluntary based on the employee's own protection needs and financial considerations.

There is no change for foreign employees.

Participation remains mandatory under the current regulations.

PERKESO has opened an online self-service system for local employees to submit their participation decision.

Select:

"SAYA MEMILIH UNTUK MENYERTAI"

If you are employed by more than one employer, you will also need to choose which employer will be responsible for the scheme contribution.

Select:

"SAYA MEMILIH UNTUK TIDAK MENYERTAI"

Employees who choose to opt out must complete the Borang Perakuan Pelepasan Liabiliti (Declaration of Release of Liability).

This declaration confirms that the employee understands they will no longer be entitled to claim benefits under the LINDUNG 24 JAM scheme for eligible non-work-related accidents.

Visit the official PERKESO LINDUNG Faedah Portal:

https://lindungfaedah.perkeso.gov.my/auth/

First-time users should click:

Daftar Akaun (Register Account)

Prepare the following information:

Full Name

NRIC Number

Email Address

Password

Log in to your newly created account.

Go to the participation page and choose either:

✅ SAYA MEMILIH UNTUK MENYERTAI

or

❌ SAYA MEMILIH UNTUK TIDAK MENYERTAI

Carefully verify your information, including:

Personal details

NRIC number

Employer information

Participation status

Selected employer (if applicable)

Confirm and submit your declaration.

Download your Declaration Form after successful submission.

Make sure the declaration correctly reflects:

Your personal information

Employer information

Participation status

Submission date

According to PERKESO's current online process, your submitted declaration will be treated as your official decision.

Before clicking Submit, ensure all information is accurate.

Employees should understand that:

Participation provides additional protection for eligible non-work-related accidents.

Employees who opt out will no longer be covered under this scheme.

A Declaration of Release of Liability is required for those opting out.

Foreign employees are not eligible to opt out.

Although the participation decision is made by the employee, employers and HR teams still play an important role in ensuring proper implementation.

Employers should:

Inform employees about the latest policy update

Guide employees on using the official portal

Keep copies of employees' declarations

Update payroll records where necessary

Avoid incorrect deductions or omissions

Handle employees with multiple employers appropriately

Explain the implications of opting in or opting out

Employers should not make participation decisions on behalf of employees without a properly completed declaration.

Since the scheme was initially implemented in June 2026, some employers may have already made salary deductions based on the previous mandatory requirement.

For any adjustments relating to payroll, contribution handling, or implementation dates following an employee's opt-out, employers should follow PERKESO's latest instructions and future announcements.

HR and Payroll teams are advised not to make assumptions regarding refunds or deduction adjustments without official guidance.

Although participation is now voluntary for local employees, the scheme continues to provide additional social protection outside normal working hours.

Potential benefits include:

Protection against eligible non-work-related accidents

Financial assistance for qualifying incidents

Additional protection beyond workplace accident coverage

Extra support for employees without personal accident insurance

Before deciding to opt out, employees should consider their existing insurance coverage, such as:

Medical Insurance

Personal Accident Insurance

Income Protection Plans

Personal financial commitments

This policy change does not mean employers can simply ignore the scheme.

Companies should continue to:

✅ Inform employees of the latest requirements

✅ Guide employees through the online submission process

✅ Keep proper documentation

✅ Update payroll procedures

✅ Differentiate between local and foreign employees

✅ Stay updated with future PERKESO announcements

Failure to maintain proper records or process payroll correctly could expose employers to unnecessary compliance risks.

The latest implementation can be summarised as follows:

Eligible local employees may submit their decision through PERKESO's official online portal from 13 July 2026 onwards.

Both employees and employers should understand the implications of participation before making any decision and ensure all records are properly maintained.

If your company requires assistance with Payroll, PERKESO compliance, statutory contributions, or HR advisory services, HBA Global Consultancy is here to help.

This article is intended for general informational purposes only and should not be considered legal, HR, insurance, or professional compliance advice. Policies, procedures, and implementation mechanisms may change based on future announcements by the Ministry of Human Resources (KESUMA) or PERKESO. Employers and employees should always refer to the latest official guidelines before making any decisions.

The information provided in this article is intended for general educational and informational purposes only. While every effort has been made to ensure the accuracy of the information at the time of publication, tax laws, reliefs, eligibility criteria, administrative practices, and implementation guidelines may be revised, updated, or clarified by the Inland Revenue Board of Malaysia (LHDN) from time to time.

The tax reliefs, limits, examples, and explanations discussed in this article are based on publicly available information relating to Budget 2026 proposals and announcements. The actual eligibility, qualifying conditions, supporting documentation requirements, and claim procedures may vary depending on an individual's circumstances and the latest guidance issued by LHDN.

Readers are strongly advised to refer to the latest official publications, guidelines, FAQs, Public Rulings, and announcements issued by LHDN before making any tax-related decisions or submitting their income tax returns.

This article should not be construed as tax, legal, financial, or professional advice. HBA Global Consultancy Sdn. Bhd. shall not be held responsible for any loss, liability, or consequences arising from reliance on the information contained in this article without obtaining professional advice tailored to specific circumstances.

For the most up-to-date information, please refer directly to LHDN's official website and published guidance.

随着 2026 年已经过半,许多纳税人可能已经在某些项目上消费,却不知道这些开销有机会在明年报税时申请税务减免(Tax Relief)。

每年马来西亚财政预算案(Budget)都会针对个人所得税减免项目作出调整。有些更新广受关注,但也有不少新措施往往要等到报税季来临时,大家才发现自己原来符合资格。

然而到了报税时,许多人却发现:

收据(Receipt)已经遗失

e-Invoice 找不到了

支持文件不完整

为了让大家提早做好准备,我们整理了 Budget 2026 中 6 项值得关注的税务减免更新。

过去,只有指定疫苗符合税务减免资格。

从 2026 估税年(YA 2026)开始,减免范围扩大至所有获得国家药剂监管局(NPRA)批准的疫苗。

例如:

流感疫苗(Influenza)

骨痛热症疫苗(Dengue)

HPV 疫苗

肺炎球菌疫苗(Pneumococcal)

其他经 NPRA 批准的疫苗

此项减免属于医疗费用相关减免项目,纳税人只需保留完整的付款记录及相关证明文件,即有机会申请税务减免。

对于有孩子的家庭来说,这是一项值得关注的更新。

过去,税务减免一般仅适用于:

注册托儿所(TASKA)

幼儿园(TADIKA)

从 YA 2026 开始,以下机构也纳入减免范围:

Day Care Centre(托管中心)

Transit Centre(安亲班)

这项调整有助于减轻双薪家庭及需要课后照顾服务家庭的经济负担。

建议家长妥善保存相关学费收据及付款记录,以便未来报税时使用。

这是许多人容易忽略的一项更新。

过去,人寿保险税务减免主要适用于:

纳税人本人

配偶

从 YA 2026 开始,符合资格的孩子人寿保险(Life Insurance)及伊斯兰保险(Takaful)保费,也可纳入现有减免范围。

需要特别注意的是:

这并不是新增 RM3,000 的减免项目,而是现有 RM3,000 人寿保险减免的适用范围扩大至符合条件的孩子。

因此,家长应妥善保留保单及保费付款记录,以备报税时申报。

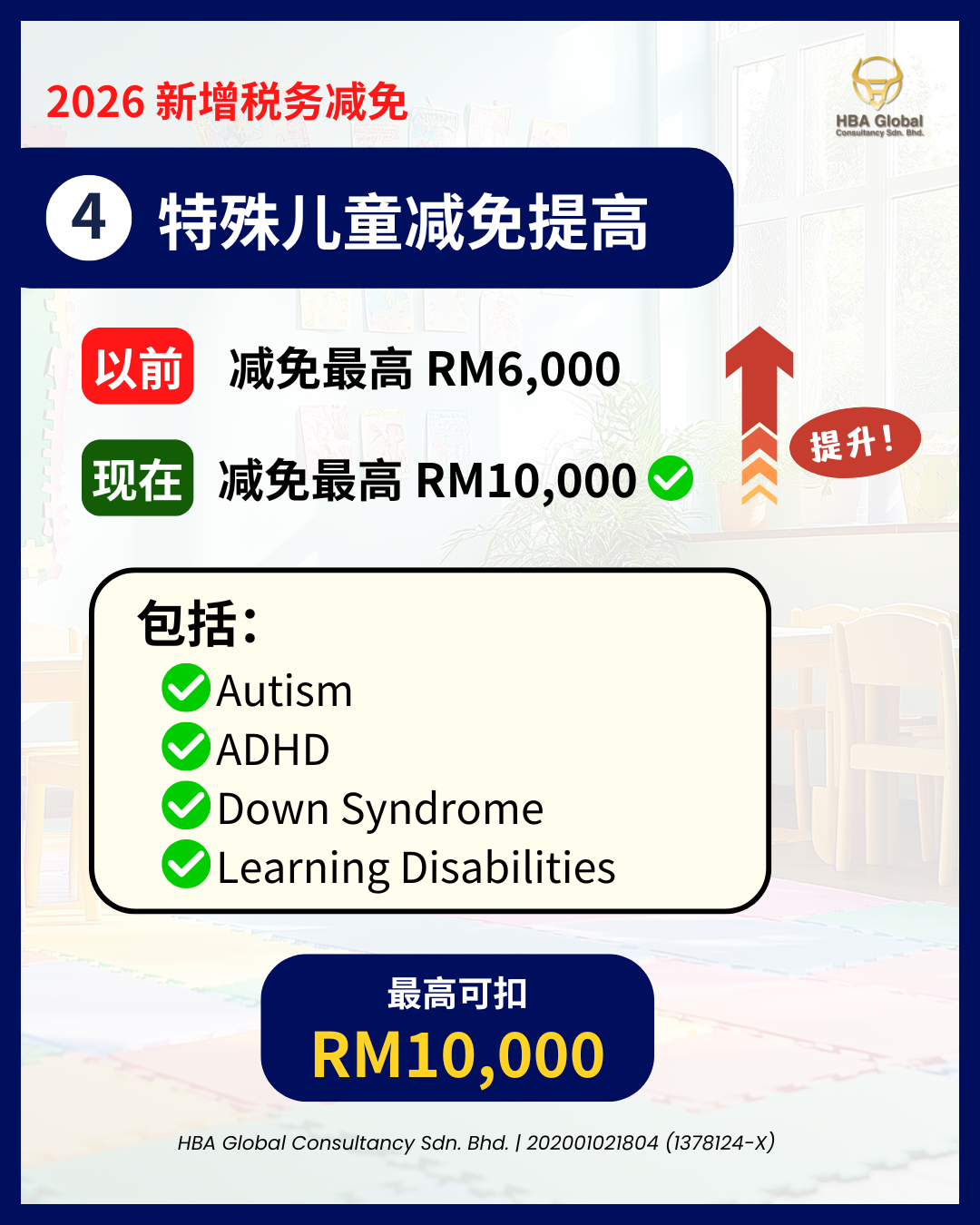

照顾特殊需求儿童的家庭将获得更高的税务减免。

减免金额由原本的:

RM6,000

提高至:

RM10,000

适用于符合资格的情况,例如:

自闭症(Autism Spectrum Disorder)

过动症(ADHD)

唐氏综合症(Down Syndrome)

发育迟缓(Global Developmental Delay)

学习障碍(Learning Disabilities)

其他获认可的发展障碍

这项提升反映政府持续加强对特殊家庭的支持。

Budget 2026 也为家庭用户带来一项实用更新。

以下项目现已纳入相关税务减免范围:

Home CCTV(家居闭路电视)

Food Waste Grinder(厨余粉碎机)

此前符合资格的项目包括:

电动车充电器(EV Charger)

厨余堆肥机(Food Waste Composting Machine)

如果您计划提升家居安全或改善环保设施,记得保留购买发票及安装记录。

配合 2026 马来西亚旅游年(Visit Malaysia Year 2026),政府新增部分国内旅游相关减免。

符合资格的景点包括:

主题乐园(Theme Park)

动物园(Zoo)

博物馆(Museum)

国家公园(National Park)

海洋公园(Marine Park)

文化活动(Cultural Programme)

换句话说,部分休闲娱乐活动除了丰富生活体验,也可能帮助您获得税务减免。

建议保留门票、付款记录及相关文件作为支持资料。

许多纳税人最大的错误,就是等到报税季才开始整理资料。

到了那个时候:

❌ 收据不见了

❌ e-Invoice 被删除了

❌ 银行记录找不到了

最好的做法,是从现在开始建立专属资料夹,无论是实体文件夹或电子档案夹,都能帮助您更有效管理相关文件。

针对 YA 2026,建议保留以下资料:

疫苗费用收据

安亲班及托管中心收费记录

孩子保险保费记录

特殊儿童相关医疗及教育费用文件

Home CCTV 购买记录

国内旅游景点门票

e-Invoice

收据及付款证明

根据马来西亚税务规定,相关文件一般应保存至少七年。

税务减免看似只是报税过程中的一个小环节,但若善加利用,往往能够有效降低应课税收入。

重点不是等到明年报税时才研究,而是从现在开始了解相关政策,并妥善保存文件。

这样不仅能避免遗漏符合资格的减免项目,也能让未来报税过程更加顺利。

如果您不确定某项开销是否符合税务减免资格,建议在报税前咨询专业税务顾问。

HBA Global Consultancy 致力于协助个人及企业了解税务责任,并在符合 LHDN 规定的前提下,善用合法税务减免。

我们拥有超过 12 年经验,并服务接近 800 家企业。

✔ 会计服务(Accounting)

✔ 税务服务(Tax)

✔ 公司秘书服务(Company Secretary)

✔ 审计服务(Audit)

欢迎联系我们了解更多详情。

本文内容仅供一般教育及资讯用途参考。

尽管我们已尽力确保本文发布时所载资料的准确性,但税务法令、税务减免项目、资格条件、行政程序及执行指南可能会因马来西亚内陆税收局(LHDN)后续公布的最新指南、常见问题(FAQ)、公共裁决(Public Ruling)或其他官方公告而有所修改、更新或进一步说明。

本文所提及的税务减免项目、限额、案例及解释,均依据 Budget 2026 公布资料及公开信息整理。实际适用资格、申报条件、所需支持文件及申请方式,仍须以 LHDN 最新官方指南为准。

读者在作出任何税务决定或提交报税表前,建议查阅 LHDN 最新发布的官方资料及相关指南。

本文内容不构成税务、法律、财务或其他专业意见。HBA Global Consultancy Sdn. Bhd. 对因依赖本文内容而产生的任何损失、责任或后果概不负责。

如需最新及最准确的信息,请以 LHDN 官方网站及最新发布文件为准。

As we move through 2026, many taxpayers may already be spending on items that qualify for tax relief without realizing it.

Every year, Malaysia's Budget introduces changes to personal income tax reliefs. Some updates receive significant attention, while others go unnoticed until tax filing season arrives.

By then, many taxpayers discover that receipts have been misplaced, e-Invoices cannot be found, or supporting documents are incomplete.

To help you prepare early, here are six notable tax relief updates introduced under Budget 2026.

Previously, only selected vaccines qualified for tax relief.

For YA 2026, the scope has been expanded to include vaccines approved by the National Pharmaceutical Regulatory Agency (NPRA).

Examples include:

Influenza Vaccine

Dengue Vaccine

HPV Vaccine

Pneumococcal Vaccine

Other approved vaccines

This relief falls under the medical expenses category and may help reduce your taxable income when supported by proper documentation.

Working parents may benefit from this update.

Previously, tax relief was generally available for fees paid to registered childcare centres (TASKA) and kindergartens (TADIKA).

The relief now includes:

Day Care Centres

Transit Centres

This expansion provides additional support for parents who rely on after-school care services for their children.

Be sure to keep payment records and receipts issued by the childcare provider.

One of the lesser-known updates involves life insurance tax relief.

Previously, the relief mainly covered insurance premiums relating to the taxpayer and spouse.

Under the updated rules, eligible premiums paid for children's life insurance and children's takaful plans may also qualify under the existing relief framework.

It is important to understand that this is not a new relief category. Instead, the scope of the existing relief has been expanded.

Parents are encouraged to retain policy documents and premium payment records for future tax filing purposes.

Families caring for children with special needs will benefit from an increased relief amount.

The allowable relief has been increased from RM6,000 to RM10,000.

This applies to qualifying conditions such as:

Autism Spectrum Disorder (ASD)

Attention Deficit Hyperactivity Disorder (ADHD)

Down Syndrome

Global Developmental Delay (GDD)

Learning Disabilities

Other recognised developmental conditions

This enhancement reflects the government's continued effort to support families facing higher medical and educational expenses.

Budget 2026 also introduces a practical update for homeowners.

The following items may now qualify under the relevant tax relief category:

Home CCTV Systems

Food Waste Grinders

These are in addition to previously eligible items such as electric vehicle chargers and food waste composting machines.

If you are planning home security or sustainability improvements, remember to retain the purchase invoice and installation records.

In conjunction with Visit Malaysia Year 2026, selected tourism-related expenses may qualify for tax relief.

Examples include:

Theme Parks

Zoos

Museums

National Parks

Marine Parks

Cultural Programmes

Certain leisure activities may therefore contribute towards tax savings while supporting Malaysia's tourism industry.

Taxpayers should retain tickets, receipts, and payment records as supporting documents.

One of the most common mistakes taxpayers make is waiting until tax filing season before reviewing their expenses.

By that time:

Receipts may have been misplaced

e-Invoices may have been deleted

Payment records may be difficult to retrieve

The best approach is to create a dedicated folder, either physical or digital, and store all relevant tax documents throughout the year.

For YA 2026, consider keeping records for:

Vaccination Expenses

Childcare and Transit Centre Fees

Children's Insurance Premiums

Special Needs Child Treatment Expenses

Home CCTV Purchases

Domestic Tourism Attraction Tickets

e-Invoices

Payment Receipts

Under Malaysian tax regulations, supporting documents should generally be retained for at least seven years.

Tax reliefs may seem like a small part of financial planning, but they can significantly reduce your taxable income when utilised correctly.

The key is preparation.

Understanding the available tax reliefs now allows you to make informed spending decisions and avoid missing out on legitimate tax savings later.

If you are unsure whether a particular expense qualifies for tax relief, it is always advisable to seek professional tax advice before filing your tax return.

At HBA Global Consultancy, we assist individuals and businesses in understanding their tax obligations while maximising available tax reliefs in compliance with LHDN requirements.

With more than 12 years of experience and nearly 800 businesses served, our team is ready to help.

✔ Accounting

✔ Tax

✔ Company Secretary

✔ Audit

Contact us today to learn more.

The information provided in this article is intended for general educational and informational purposes only. While every effort has been made to ensure the accuracy of the information at the time of publication, tax laws, reliefs, eligibility criteria, administrative practices, and implementation guidelines may be revised, updated, or clarified by the Inland Revenue Board of Malaysia (LHDN) from time to time.

The tax reliefs, limits, examples, and explanations discussed in this article are based on publicly available information relating to Budget 2026 proposals and announcements. The actual eligibility, qualifying conditions, supporting documentation requirements, and claim procedures may vary depending on an individual's circumstances and the latest guidance issued by LHDN.

Readers are strongly advised to refer to the latest official publications, guidelines, FAQs, Public Rulings, and announcements issued by LHDN before making any tax-related decisions or submitting their income tax returns.

This article should not be construed as tax, legal, financial, or professional advice. HBA Global Consultancy Sdn. Bhd. shall not be held responsible for any loss, liability, or consequences arising from reliance on the information contained in this article without obtaining professional advice tailored to specific circumstances.

For the most up-to-date information, please refer directly to LHDN's official website and published guidance.

Published: June 2026

Environmental, Social and Governance (ESG) reporting is becoming increasingly important worldwide, and Malaysia is now taking steps towards introducing sustainability reporting requirements under the Companies Act 2016.

On 30 April 2026, the Companies Commission of Malaysia (SSM) released a Consultative Document on the Proposed Amendments to the Companies Act 2016 relating to Sustainability Reporting.

While many SMEs may assume ESG only affects large corporations, the proposed roadmap suggests that sustainability reporting requirements could gradually expand to cover more businesses in the future.

ESG stands for:

How a company manages its impact on the environment.

Examples:

Energy consumption

Waste management

Carbon emissions

Recycling initiatives

How a company manages relationships with employees, customers, and communities.

Examples:

Employee welfare

Workplace safety

Diversity and inclusion

Community involvement

How a company is managed and controlled.

Examples:

Internal controls

Ethical business practices

Risk management

Board oversight

")

According to SSM's consultation paper, sustainability reporting requirements may be introduced in phases based on company size.

Expected from 2028 onwards:

Revenue between RM1 billion and RM2 billion; or

500 employees or more

Expected from 2030 onwards:

Revenue between RM100 million and RM1 billion; or

250 to 499 employees

Expected from 2032 onwards:

Revenue between RM15 million and RM100 million; or

100 to 249 employees

Companies below:

RM15 million revenue; or

100 employees

are currently not proposed to be subject to mandatory sustainability reporting requirements, although voluntary adoption is encouraged.

Many SME owners may think:

"My company is not required to submit ESG reports, so why should I bother?"

The reality is that ESG is no longer just about compliance.

Large companies, multinational corporations, banks, investors and government-linked organisations are increasingly requesting ESG-related information from suppliers and business partners.

Even if ESG reporting is not mandatory for your company today, you may be asked for ESG information when:

Applying for financing

Participating in tenders

Becoming a supplier to larger corporations

Working with multinational companies

Seeking investment opportunities

The trend is clear.

In the future, companies may be evaluated not only on:

✔ Revenue

✔ Profitability

But also on:

✔ Employee welfare

✔ Sustainability initiatives

✔ Corporate governance

✔ Business ethics

✔ Risk management practices

Businesses that prepare early may gain a competitive advantage.

")

You do not need a complex ESG report immediately.

Instead, SMEs can begin with simple steps:

Track electricity and water usage

Reduce paper consumption

Implement recycling initiatives

Improve employee training

Review workplace safety practices

Encourage staff engagement activities

Document internal policies

Strengthen approval procedures

Improve financial transparency

These are often the building blocks of future ESG reporting.

Although mandatory reporting for most SMEs may still be several years away, business owners should start understanding:

What ESG means

How ESG affects financing and tenders

What sustainability data should be tracked

How governance practices can be improved

Early preparation is often easier and more cost-effective than rushing to comply later.

SSM's proposed sustainability reporting framework signals a significant shift in Malaysia's corporate reporting landscape.

While most SMEs are not expected to face mandatory reporting requirements immediately, ESG is increasingly becoming part of how businesses are assessed by customers, investors, banks, and regulators.

The question is no longer:

"Do I need ESG today?"

But rather:

"Am I prepared when ESG becomes a business expectation tomorrow?"

At HBA Global Consultancy, we work with experienced ESG professionals who can assist businesses in understanding ESG requirements, building sustainability awareness, and preparing practical ESG frameworks suitable for SMEs.

Whether you are just starting your ESG journey or looking to strengthen your sustainability practices, our team is ready to help.

📞 Contact HBA Global Consultancy today to learn more about ESG readiness and sustainability reporting.

Many taxpayers have recently logged into MyTax and discovered a document called:

📄 CP500 (Tax Instalment Notice)

Their first reaction is often:

👉 Why am I suddenly being asked to pay tax?

👉 Didn’t I already file my income tax return?

👉 Is CP500 a new type of tax?

The answer is no.

CP500 is not a new tax. It is a tax instalment mechanism introduced by LHDN to collect tax in advance from individuals with certain types of non-employment income.

CP500 is a notice issued by LHDN based on your previous year's tax filings.

LHDN estimates your tax payable for the current year and requires you to pay it in instalments throughout the year instead of making a lump-sum payment later.

In simple terms:

📌 Rather than paying all your taxes after filing your return,

📌 You pay the estimated tax in advance through scheduled instalments.

Typically, the instalments are divided into six payments per year.

CP500 commonly applies to individuals who earn income other than regular employment income, such as:

✅ Rental income

✅ Commission income

✅ Insurance agents

✅ Property agents

✅ Freelancers

✅ Online business owners

✅ Sole proprietors

✅ Individuals with side-income activities

Since these income sources are generally not subject to monthly tax deductions (PCB), LHDN may issue a CP500 notice to collect tax progressively.

If you have declared non-employment income in previous years, such as:

✔ Rental income

✔ Commission income

✔ Freelance income

✔ Royalties

✔ Interest income

LHDN may classify you under the CP500 tax instalment system.

This helps taxpayers spread out their tax payments and reduces the risk of a large tax bill at the end of the year.

One of the most discussed tax updates recently is LHDN's announcement regarding a CP500 penalty exemption for certain taxpayers.

Under this special arrangement, eligible taxpayers may not be subject to CP500 late-payment penalties even if they do not pay the instalments according to schedule.

The exemption is primarily intended for individuals who:

✅ Have employment income; and

✅ Also earn non-employment income.

Examples include:

Employees who earn rental income

Employees who do freelance work

Employees who receive insurance commissions

Employees who earn royalty income

The purpose is to provide a transition period for taxpayers who are newly introduced to the CP500 system.

Many taxpayers misunderstand the announcement and assume:

❌ "I received CP500, so I don't need to pay."

This is incorrect.

The exemption does not automatically apply to everyone.

Individuals whose primary income consists of:

Business income

Self-employment income

Rental income

Commission income

may still be subject to the normal CP500 requirements and penalties.

Always verify your eligibility before assuming the exemption applies to you.

If your income has decreased significantly during the year, you may apply to revise your instalment amount through:

📄 Form CP502

Common situations include:

✔ Business slowdown

✔ Vacant rental properties

✔ Reduced commissions

✔ Discontinued side businesses

Submitting CP502 allows you to request a lower CP500 instalment amount based on your current circumstances.

Even if you qualify for a CP500 penalty exemption, there is something important to remember:

⚠️ CP500 penalty exemption does NOT mean all tax penalties are waived.

If you file your tax return and still have outstanding tax payable, failure to settle the balance by the prescribed deadline may still result in:

❌ 10% late payment penalty

Therefore, taxpayers should continue monitoring their overall tax position and payment obligations.

If you receive a CP500 notice, don't rush to pay it — but don't ignore it either.

Take the time to understand:

✔ Why you received the notice

✔ Whether you qualify for any exemption

✔ Whether the instalment amount is reasonable

✔ Whether a CP502 adjustment is necessary

Proper tax planning can help:

✅ Improve cash flow management

✅ Avoid unnecessary tax burdens

✅ Reduce future penalties and tax issues

✅ Ensure compliance with LHDN requirements

LHDN CP500 Tax Instalment Information

https://www.hasil.gov.my

MyTax Portal

https://mytax.hasil.gov.my

This article is for general informational purposes only and does not constitute professional tax advice. Tax treatment may vary depending on individual circumstances and future LHDN updates. Professional advice should be sought before making tax-related decisions.

🇲🇾 HBA Global Consultancy

🔥 Accounting

🔥 Tax

🔥 Company Secretary

🔥 Audit

📞 Need assistance with CP500, personal tax planning, or tax compliance? Contact our team today.

近年来,不少纳税人在登入 MyTax 时发现自己收到了一份来自 LHDN 的文件:

📄 CP500(Notis Bayaran Ansuran)

很多人的第一反应是:

👉 为什么突然要我缴税?

👉 我不是已经报税了吗?

👉 CP500 是新的税吗?

其实,CP500 并不是新税种,而是一种 预缴税款(Tax Instalment)机制。

CP500 是 LHDN 根据你过往申报的收入情况,预估你下一年度应缴纳的税款,并要求你分期预先缴付税款。

简单来说:

不是等到明年报税才一次过缴税,

而是提前分成 6 期缴纳。

常见适用人士包括:

✅ 房东(Rental Income)

✅ 自由工作者(Freelancer)

✅ 保险代理员

✅ 房地产代理员

✅ 网卖卖家

✅ 拥有副业收入的人士

✅ Sole Proprietor 业主

如果你除了薪水之外,还有其他收入来源,例如:

✔ 租金收入

✔ 佣金收入

✔ 副业收入

✔ 版权费

✔ 利息收入

LHDN 可能会发出 CP500 通知。

因为这些收入不像薪水一样有 PCB(每月预扣税),所以税务局会要求你提前缴税。

近期 LHDN 宣布:

部分符合条件的纳税人,即使没有按照 CP500 时间表缴付税款,也不会被征收 CP500 迟缴罚款。

这项豁免主要适用于:

✅ 有就业收入(Employment Income)

同时

✅ 也有非就业收入(Non-Employment Income)的人士

例如:

上班族 + 收租金

上班族 + 接 Freelance

上班族 + 保险佣金

上班族 + 版权收入

政府表示,这项安排主要是给予纳税人适应 CP500 制度的过渡期。

很多人误会:

❌ 收到 CP500 = 今年不用缴税

这是错误的。

根据 LHDN 说明:

如果你的收入主要来自:

生意收入

自雇收入

租金收入

佣金收入

且本来就属于 CP500 群体,

则未必自动享有这项过渡性豁免。

如果今年收入明显下降:

✔ 生意变差

✔ 房子空租

✔ 停止副业

✔ 停止收取佣金

可以透过:

📄 Form CP502

向 LHDN 申请调整 CP500 金额。

2026 年的调整期限为:

📅 第一次:30 June 2026

📅 第二次:31 October 2026

虽然部分人士可享 CP500 罚款豁免,

但很多人忽略了一点:

👉 CP500 罚款豁免 ≠ 所有税务罚款豁免

如果你最终报税后仍有税款需要缴付,

但没有在规定期限内付款,

仍可能面对迟缴罚款。

收到 CP500 时,不要急着缴,也不要直接忽略。

建议先确认:

✔ 为什么收到 CP500

✔ 是否属于豁免群体

✔ 金额是否合理

✔ 是否需要提交 CP502 调整

因为处理正确的话:

👉 可以改善现金流规划

👉 避免不必要的税务负担

👉 降低未来被追税或罚款的风险

LHDN CP500 Tax Estimation Advance Payment

https://www.hasil.gov.my/en/individual/individual-life-cycle/payment/tax-estimation-advance-payment/

MyTax Portal

https://mytax.hasil.gov.my

本文仅供一般资讯参考,不构成税务建议。实际税务处理应根据纳税人的具体情况及 LHDN 最新规定而定。如需专业协助,建议咨询合格税务顾问。

Recently, many employers and employees have been asking:

“Will paid maternity leave in Malaysia increase from 98 days to 128 days in 2026?”

“Who pays for the additional 30 days?”

“Will employers have to bear an extra month of salary?”

The topic has generated significant attention, but it is important to clarify one key point:

The Employment Act 1955 has not been amended to increase statutory maternity leave from 98 days to 128 days.

A more accurate explanation is:

98 days of statutory paid maternity leave + up to 30 days of post-maternity financial support = a potential postnatal recovery period of up to 128 days.

Under the Employment Act 1955, eligible female employees are entitled to 98 consecutive days of paid maternity leave.

This entitlement has been in effect since 1 January 2023 and is not a new provision introduced in 2026.

The 98-day period is counted continuously, meaning that weekends, rest days, and public holidays are generally included within the maternity leave period.

The new development attracting attention is the government's proposal to introduce:

Elaun Pasca Cuti Bersalin (EPCB)

Post-Maternity Leave Allowance

The purpose of this initiative is to provide additional financial support to eligible female employees who require extra recovery time after completing their statutory maternity leave.

Based on information currently available, the allowance may provide:

Up to 30 additional days of support

Approximately 80% of the employee's monthly salary

A payment made through the proposed allowance mechanism

It can be understood as follows:

However, employers should avoid telling employees that:

❌ "Maternity leave has officially increased to 128 days."

A more accurate statement would be:

✅ "Under the proposed 2026 Post-Maternity Leave Allowance, eligible female employees may receive up to 30 additional days of financial support after completing their 98-day maternity leave, resulting in a potential recovery period of up to 128 days."

This distinction is important because the statutory maternity leave entitlement remains at 98 days, while the additional 30 days is expected to be supported through a separate allowance mechanism.

Assume a female employee earns RM5,000 per month and satisfies all eligibility requirements.

During the statutory maternity leave period:

The employee enjoys 98 consecutive days of paid maternity leave.

Salary continues to be paid according to existing legal requirements.

In simple terms:

98 Days Maternity Leave = Normal Salary Paid

If the employee qualifies for EPCB after completing the 98-day maternity leave period:

Monthly Salary: RM5,000

80% Allowance Rate:

RM5,000 × 80% = RM4,000

The employee may therefore receive approximately RM4,000 in additional post-maternity support for the extra 30-day period.

Therefore, when people say "paid maternity leave has increased to 128 days", the more accurate explanation is:

98 days of statutory paid maternity leave + up to 30 days of post-maternity allowance support = up to 128 days of postnatal recovery time.

This does not automatically mean employers must pay 128 days of full salary.

One of the most common concerns among employers is:

"Will the company have to pay an extra 30 days of salary?"

Based on current announcements, the EPCB proposal is expected to be introduced through amendments related to the Employment Insurance System (EIS) framework.

The objective is to provide financial assistance through a social protection mechanism rather than transferring the entire additional cost directly to employers.

As a result, employers should focus on:

Monitoring official announcements

Understanding eligibility requirements

Reviewing future implementation procedures

rather than assuming they will automatically bear an additional 30 days of full salary costs.

Based on information currently available, eligible female employees may generally include those who:

Have worked for at least 90 days within the 9 months preceding childbirth;

Have been employed for at least one day during the four months immediately before childbirth;

Have fewer than five surviving children at the time of delivery; and

Are insured employees under the relevant social protection scheme.

Final eligibility requirements remain subject to official government guidelines.

The proposed allowance aims to:

Provide additional recovery time for mothers after childbirth;

Encourage female workforce participation;

Reduce the number of women leaving employment after maternity leave;

Support long-term career continuity for working mothers.

In other words, the initiative is not simply about extending leave but about improving support for women returning to the workforce after childbirth.

For SMEs and employers, this development is worth preparing for early.

Companies should review:

Are maternity leave policies clearly stated?

Do contracts include updated maternity leave provisions?

Can payroll accurately distinguish between maternity leave payments and allowance-related support?

Does the HR team understand the difference between the statutory 98-day leave and the proposed 30-day allowance?

Will company procedures need updating once EPCB is officially implemented?

Businesses with female employees should not wait until an employee is about to go on maternity leave before addressing these issues.

The key message is simple:

Malaysia is not increasing statutory maternity leave from 98 days to 128 days.

Instead:

Female employees already enjoy 98 days of paid maternity leave. The proposed 2026 Post-Maternity Leave Allowance may provide eligible employees with up to 30 additional days of support at approximately 80% of salary, resulting in a potential recovery period of up to 128 days.

The reason this topic has attracted so much attention is because of the government's proposal to introduce the Post-Maternity Leave Allowance (EPCB).

If implemented, the allowance could provide eligible female employees with up to:

30 additional days of support

Approximately 80% salary replacement

Enhanced postnatal financial protection

For employees, this offers greater support during recovery after childbirth.

For employers, it represents an important HR, payroll, and compliance development that should be monitored closely.

Businesses should stay updated on official government announcements and review their internal policies early to avoid misunderstandings regarding maternity leave entitlements, salary payments, and employee rights.

🇲🇾 With over 12 years of experience and nearly 800 businesses served, HBA Global Consultancy is here to help.

🔥 Accounting

🔥 Tax

🔥 Company Secretary

🔥 Audit

📞 Need professional advice? Contact us today.